Boris, Brexit and the Hedge Funds (Part 1)

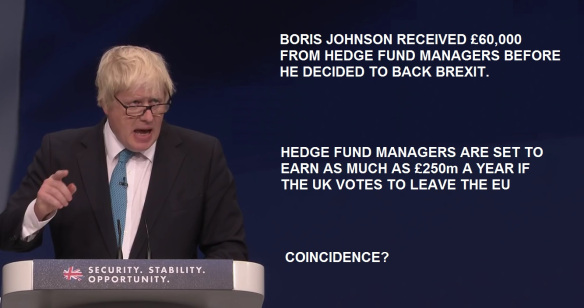

WHO does Boris Johnson really represent? Put another way, which groups in society fund a hard Brexit and Boris Johnson’s election campaign. The answer is a specific splinter group of City finance capitalists who run so-called “hedge funds”. Among the City hedge fund operators backing Boris are David Lilley of RK Capital, Jon Wood of SRM Global, and Johan Christofferson of Christofferson, Robb and Co.

WHO does Boris Johnson really represent? Put another way, which groups in society fund a hard Brexit and Boris Johnson’s election campaign. The answer is a specific splinter group of City finance capitalists who run so-called “hedge funds”. Among the City hedge fund operators backing Boris are David Lilley of RK Capital, Jon Wood of SRM Global, and Johan Christofferson of Christofferson, Robb and Co.*

The term “hedge fund” was originated in the 1940s by a maverick Australian (later American) investor called Alfred Winslow Jones. He invented a new kind of fund that “hedged” its investment bets by offsetting growth stocks by short-selling others. Jones made money whether the market went up or down. A modern hedge fund does the same thing, but on a giant scale.

*

But these are not “normal” investment funds, like a pension fund or a mutual trust. The latter put money from small savers into safe assets like bonds and FTSE 100 company shares. Hedge funds, on the other hand, are risk-takers. They invest in risky stocks or projects, with the intent to make above-average returns. Example: in 2018, a UK hedge called Odey Asset Management made a return (in one year) of a staggering 53 per cent. Odey is run by arch-Brexiteer Crispin Odey, one of Boris Johnson’s most sycophantic financial backers.

*

You do not make insane returns Odey’s merely by guessing correctly. Markets are crazy things that nobody can predict. Instead, hedge funds spread multiple big bets, aiming to offset bad risks in one area by getting lucky somewhere else. This involves rigging markets, but in a perfectly legal way. This rigging involves “shorting”.

*

Crudely, shorting means borrowing shares (for a small fee) that the hedge fund thinks will decrease in value. The hedge fund then sells these borrowed shares to buyers willing to pay the current market price (or a wee bit lower to get interest). When (if) the share eventually price drops, the hedge fund can re-purchase them at the lower cost, return the borrowed shares and pocket the difference.

*

The magic in all this is that the very act of “shorting” a given stock often sends its share price falling through the floor, as the rest of the market panics. It’s as if betting on a particular horse to lose actually causes it to stumble. Hedge funds make their cash not by shoring one particular stock but by betting on huge trends. For instance, Odey Asset Management – friend to Boris – has been actively shorting lots of UK high street retail chains. It does not take any brains to know high street shops are in trouble from the switch to internet purchases. But Odey is busy shorting their shares wholesale, which only makes matters worse – even for retailers that are doing ok. This is why hedge funds are poisonous.

*

In effect, hedge funds are a kind of bet spreading operation. The science (if it can be called that) is to pyramid bets so you win more than you lose. Because the risks are astronomical, hedge funds are closed to the general public. The upside is that this means they are largely unregulated. They also operate out of tax havens like the Channel Islands or Isle of Man, to avoid scrutiny. Of course, the hedge funds operations are really headquartered in Wall Street and London, but the legal fiction is they are offshore.

*

Typically, a hedge is run by investment managers who charge an annual fee (2 per cent assets) plus an enormous performance fee (20 per cent of any increase in the fund’s value). Which is why hedge fund managers end up billionaires. Interestingly, most of the key UK hedge fund billionaires come from non-establishment backgrounds, which helps explain their populist politics. Exactly what you’d expect from financial pirates.

*

You can predict there is every chance that hedge funds will be prime places to do illegal insider trading – after all, they effectively rig the markets. No surprise then that hedge fund managers get into trouble. In 2006, GLC (Europe’s largest hedge fund) and Philippe Jabre (its boss) were each fined £750,000 by the UK regulator for insider trading. Some think Mr Jabre should have gone to jail. Instead he moved to Geneva and opened a new hedge fund. Today it is one of the largest hedge funds in Switzerland, partly because Jabre shorted the entire Japanese economy after the 2011 tsunami.

*

CRISIS IN THE HEDGE FUNDS

CRISIS IN THE HEDGE FUNDS

*

Here’s the skinny: the capitalist world is short of profitable investment opportunities. Of course, humanity is still poor and diseased so rationally we should be investing to eliminate poverty and stop global warming. But those activities don’t earn the mega profits promised by the sort of financial speculation delivered by hedge funds. In addition, since the Bank Crash of 2008, central banks have used so-called quantitative easing (printing money) to hold interest rates at near zero. As a result, returns on ordinary financial investments (e.g. buying government bonds) has slumped. Which means that putting your dosh in high-risk hedge funds looks increasingly attractive.

*

Most of the world’s hedge fund cash is managed in the USA, around $2.6 trillion in total. But next comes the UK, where hedge funds manage around half a trillion dollars of assets. Hedge funds in other countries are small beer in global terms. Hong Kong, France and Canada manage only circa $50 billion each. So it is the UK hedge fund industry which is the pivot. UK funds have to outperform competitors or lose client funds either to big brother America (with its economies of scale) or upstarts in Asia. Conclusion: UK hedge funds are global sharks.

*

(For the record, there’s a small hedge fund presence in Scotland. For instance, there is Edinburgh Partners, managed by Sandy Nairn. Established in 2003, this fund has an estimated $13.5 billion under management. But managing smallish portfolios is expensive and two years ago Scotland’s most aggressive hedge fund manager, Hugh Hendry of Eclectica Asset Management, shut up shop after wrongly betting on the break-up of the EU.)

*

So far, so lucrative. But suddenly hedge funds now find themselves in trouble. Hedge funds claim that quantitative easing – which artificially boosts the value of shares and bonds – has drastically reduced the opportunities for short-selling. Also, the recent move by central banks to raise interest rates has led to a rush of money out of emerging Asian markets – where hedge funds are used to making a pile – back to America. Result: average hedge fund returns have fallen from circa 18 per cent a year during the 1990s to a pathetic 3 per cent in recent years.

*

Also, private investors are getting annoyed with the rapacious fees charged by hedge fund managers. It’s far cheaper to stick your money in a passive mutual funds, especially if hedge funds are no longer delivering big bucks. Result: Last year total hedge fund assets under management fell for the first time since the financial crisis, due to investors taking their money out.

*

HEDGE FUNDS EMBRACE POPULISM

*

What to do if you are a hedge fund manager down to your last billion? Answer: rig global politics in your favour. If that sounds improbable, remember we are talking about folk capable of shorting the entire Japanese economy in response to a natural disaster. Hedge fund managers are megalomaniacs. It goes with the territory.

*

Hedge fund managers hate conservative central banks and quantitative easing. Instead, they thrive on market chaos and gyrating asset values they can bet against. Hence the explicit support of US hedge fund managers for Trump and disruptive Trumpian economics. For instance, a key funder of both Trump and Steven Bannon’s Breitbart News is Robert Mercer, sometime co-CEO of Renaissance Technologies, a $60 billion computer-powered hedge fund. Mercer was also a major investor in Cambridge Analytica, the company at the heart of the scandal over misuse of user data collected from Facebook.

*

Next, hedge fund managers have a particular hatred of the EU because of its drive to put US and UK funds under greater regulation – hedge funds are relatively small in the eurozone countries. The EU’s new Alternative Investment Fund Managers Directive has severely limited hedge fund operations while letting the banks off relatively scot free. As a result, continental European banks have been able to nab clients (and their money) away from US and UK hedge funds. For this development, the hedge funds blame (rightly) the influence of the big German and French banks on member state governments, the European Central Bank and (above all) the European Commission.

*

A major proponent of this line is Sir Paul Marshall, the pro-Brexit co-founder of Marshall Wace, one of Europe’s leading hedge funds. Marshall argues that in France the ruling “énarques” (graduates of the elite Ecole Nationale d’Administration) are stuck in a revolving door between jobs in the big banks and jobs in government or the EU. According to Marshall, the result is that énarques like President Macron protect the interests of the big European banks. Marshall, by the way, was a prominent Lib Dem, but he donated £100,000 to the Leave campaign. Recently he made a bob or two out of shorting Carillion shares, helping put the company out of business.

*

The antipathy of UK hedge funds to EU regulation means it is no surprise that prominent fund managers such as Crispin Odey and Michael Hintze support a hard Brexit and fund Boris. Brexit is not a cry for help from the English underclass. It is a carefully stage-managed campaign by global finance capital in the form of the hedge funds. It is being orchestrated out of hedge fund self-interest and the greed of billionaires. Boris Johnson is their front man.

*

NEXT WEEK: THE HEDGE FUND CABAL BEHIND BREXIT

And so it happened with Carillion.

Story had it that HM Government fully aware of the financial mess that Carillion was in deliberately required the delay of financial impairment news so that companies, such as Black Rock Investments, who George Osborne works for, could take massive bets on the share going down.

Similar story apparently with Farage saying immediately post the close of voting on referendum night that Remain had won. Such a statement boosted Sterling as markets opened across the world. Thereafter with Farage making a similar statement early in the morning other world trading markets marked Sterling up.

Knowing however, or should one say, being in possession of detailed polling analysis that hedge fund operators such as Farage have access to, the Leave vote caused a collapse in Sterling – with traders like Odey reputed to having made £450 million on short selling.

And that quite frankly is how the elite make money. A wizard wheeze, especially when you know the result of the race ahead of time, or can influence that result.

Oh how the little people know nothing. Poverty is their birthright. All hail the big money boys and a thank you to George for giving an insight into short trading that so little of us that know anything about it.

Great pity George is not in Westminster . His analysis is riveting. Why has the media with all its expensive financial reporters not exposing these funds and their leaders?

In the case of Carillon the government were fully aware of the dire trading position that they were in.

The government knew the underlying crisis of Carillon understating costs and overstating income.

There was no interest in saving them and those in the know made a fortune shorting them.

The government was complicit in aiding the shorters make money.

Even the liquidation was an opportunity for those in the know to make money. This is how the UK government works.

No one has been prosecuted for the fictitious and fraudulent accounts that this company delivered.

No one has been prosecuted for the collapse of the Carillon pension fund. Pension scheme members who contributed all their working lives will now have to accept reduced pensions in the bitter knowledge that the Directors who presided over the collapse were paying themselves huge bonuses as the company went under.

And this, like Sports Direct, is the way that it is. Financial crime, insider dealing, it’s all part of the way that the cabal of rich and powerful run our country..

Corruption, yes financial corruption, is at the heart of the UK and it’s elite government

And like in Animal Farm the hapless populace can only look on.

A superlative piece of journalism from Mr Kerevan except for one major stumble. George states ‘ hedge fund managers have a particular hatred of the EU because of its drive to put US and UK funds under greater regulation’.

Where is the evidence that the EU want increased regulation?

Germany’s supposedly left-wing finance minister, the Social Democratic Party’s Olaf Scholz is in shenanigans overdrive to prevent just an event. He has moved heaven and earth to move such regulation from EU majority voting to unanimous voting.

Which means of course that Sturgeons pals in Ireland along with Malta, Luxembourg, Cyprus et al. can still vote down such regulation and continue as tax havens benefiting their political and global corporate elites.

In Irelands case with its vile levels of low Corporation Tax which contribute to the ongoing stealing of Scottish jobs, the weasel SNP say nowt. As in zero, nada. Brexit and Westminster are sometimes too convenient. Why the silence?

I would like independence with honour and a shred of dignity.

Not too much to ask.

So if hedge funds are parasites draining funds from the system, what are the resulting symptoms, the anaemia if you will? Presumably there is loss of productivity caused by disorder, significant sub-optimal decisions made, stress on the human cogs in the machine, and a rise in corruption as facilitation and product. Presumably there will be attempts to self-regulate to avoid killing the host, and yet some managers will still go too far even by their ingroup standards.

We see all kinds of governmental failings, yet for all the reality shows and investigative journalistic stings and whistleblowing/leaks, we see very little of real corporate governance and the kind of trading that goes on in this article. Presumably commercial secrecy is required to avoid precisely the kinds of bets for and against described here, but systematic secrecy allows corruption and insider trading to flourish. Maybe the system cannot be made to work, in theory or practice. Perhaps it is fundamentally irrational, and extremely dangerous.

George; any credit due to Private Eye which broke this story?

“Interestingly, most of the key UK hedge fund billionaires come from non-establishment backgrounds, which helps explain their populist politics. Exactly what you’d expect from financial pirates.”

Maybe this is clumsily expressed, or maybe I’m being thick, but this line seems to imply ‘non-establishment’ types are less ethical and more selfish than ‘establishment’ types, which would surely include Johnson, for one. I’m from a non-establishment background myself and have no trouble grasping the difference between right and wrong.

The article as a whole however is brilliant, lucid and deserving of universal distribution.

thanks Niall

Is this what happened with Thomas Cook

Hedge funds thrive when able to predict volatility in the markets. Hence, their desire to finance those platforms, politics and technologies that will promote volatile market swings.

Cambridge Analytica, Parler, Brexit & Trumpism – are ALL products of market manipulation.

Wealth is power and the unscrupulous will say and support anything to further their ambitions. This is why hedge fund managers will support one side and then the other. Market stability means less profit. Hence, they will help to platform extremist views and policies that will create market chaos and turmoil. Hedge funds are enablers of political and financial instability. They seldom take a leading role. They prefer to operate in the shadows, as backseat drivers & out of the public view – for as much financial gain as possible. They will present themselves as only market observers, but this is not true.

MSM and Social Media are key factors made use of in the psychological warfare required to manipulate public perceptions. Unscrupulous politicians are key to the manipulation of the public vote – at one time for policies that are against the public’s financial interests and then, at another time, for policies that are to the public’s financial gain. As far as hedge funds are concerned, the ability to successfully predict the direction of volatility is all that matters. Being a backseat enabler, but having a finger on the pulse, allows for greater accuracy and timing for market interventions and greater profitability. What happens in the mean-time to a nation’s economy or to a company’s success or failure are viewed as opportunities to make more profit, either through early investments or through the proceeds of disaster capitalism.

Money is all that matters to them. That’s their goal, their power, and their god.

I agree with every word, but how to combat the misinformation campaigns, when voices like yours just get lost in the wilderness of cyberspace?